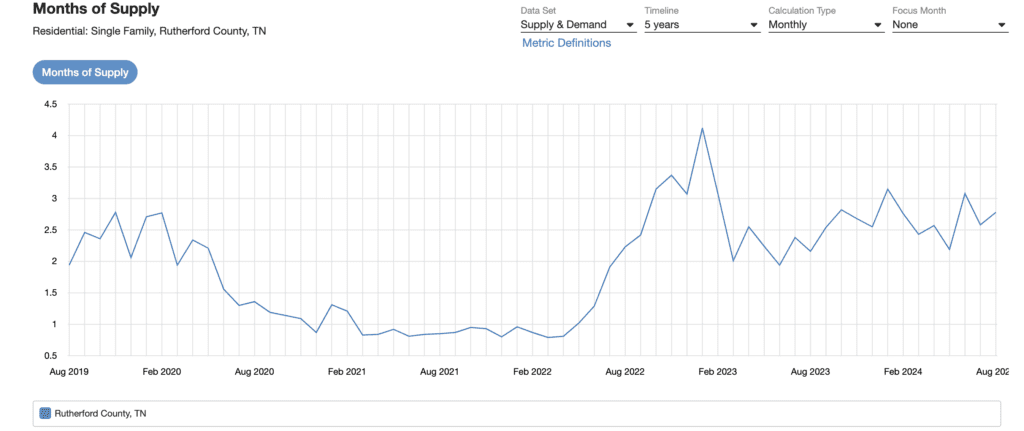

| I’ve been off on a tangent lately with my emails. Today I wanted to share some data that I look at regularly to gain an understanding of the market in general. I do keep my data to Rutherford County as that is the area I concentrate in and frankly, what happens here does not happen the same in Williamson, Marshall or Cannon Counties. Enjoy the data. If you have any thoughts or questions, give me a shout! Months of Supply–how much inventory (supply) is available calculated into a number of months given the number of closings (demand) |

| – Under 1 month Feb 21-May 22 – Returned to “normal levels” now. 2-3 months – showings down 12% since June, which was down over 10% from previous June (combined results with Showingtime and Realtracs) – Prices have tapered off since May/June, which is a seasonal expectation. Still up over same time last year. Actual inventory numbers and sales activity: |

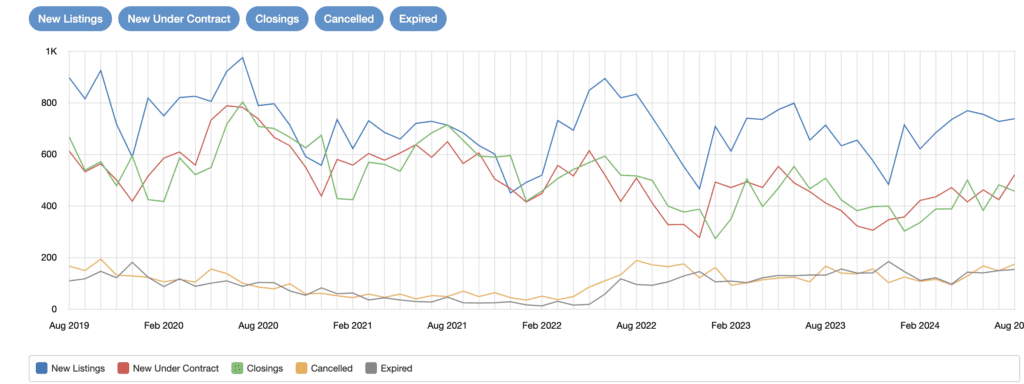

| This chart shows activity of several kinds over the past 5 years – Expired and cancelled listings have been very rare for all the last 5 years with December 2020-May of 2022 the numbers being well below 100 of each per month. Basically everything sold – The blue line shows new listings during that month. It bounces all over the place but has some spikes and troughs. Right now we are at a sustained high that is slightly lower than 2019-2022 – Notice the gap between the red and green and the blue line. Red and green pretty much travel together. From May 2020-June 2022, the gap between those two and the blue line was very narrow. After that it widened. Meaning that fewer homes were being bought as soon as they listed. That gap is much wider now than it was then. Simultaneously the orange and gray lines are up higher. This means that listings sit longer and may not sell at all–unthinkable from 2019-2022. What does that do to price? |

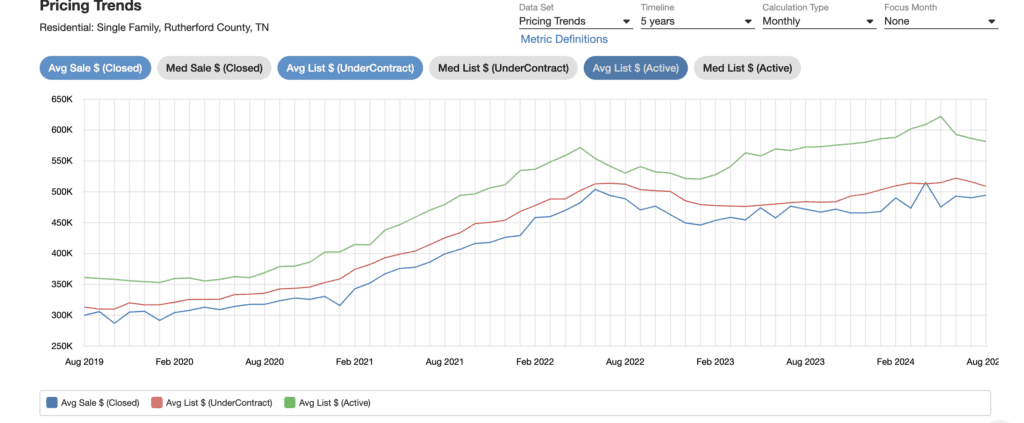

| What does this do to price? – Well, you would think the activity would drop prices. It hasn’t. We still have enough demand to keep prices up, though the rate of increase has slowed since mid-2022. – It is interesting to note the bigger gap between list and sold. See how tight that was in 2020 compared to now? – People are more negotiable and lower prices more freely just to procure a contract. Overall, we are slower. We are not losing price. We are 100% back to a seasonal market and will likely stay this way for a while. Rates have returned us to a normal market. And, exactly as I was saying for a couple of years, it feels like we’ve hit a brick wall. Really, its like we got to the end of the moving sidewalk we were running down. |